Welcome to Deflation City

Token Insight: Ponzis are making Ethereum deflationary

Quick note from me, Ben Lilly, before you start today’s piece.

I mentioned this before, but for those that are new - Espresso is changing.

What originally began as a quick 100-200 word update on the crypto market has evolved into a destination for fresh insights across crypto, macro, and traditional markets.

We look to embrace this two year progression by delivering more. To do so, we will keep introducing you to analysts that make these insights possible.

It has been over six months in the making. I can’t stress how excited we all are in terms of where this is headed. In fact, we’ve gone out of our way to become a strategic partner with an existing Web3 blogging platform to take independent research to the next level. We are literally just getting started. But more news on that later…

For now, keep enjoying Espresso as you always have. And know any new writers that emerge in the months to come have helped make what you already enjoy, possible.

So while they may seem new, you’ve already been enjoying their work.

Now without haste, ladies and gentlemen… I’d like to introduce you to our analyst that delivers some of The Labs’ most unique insights when it comes to token economies… And break dancing moves.

Welcome to the limelight, Kodi.

Ponzis are taking us to places that Ethereum has never seen before; the sunlit plains of deflation.

Yes, you heard that right. Ethereum is moving to a deflationary era. And what is behind it?

A literal Ponzi protocol with no utility is driving it.

The Ponzi in question is Xen.

The website is quite sparse, and there isn’t really that much you can do on it. There is the option to stake XEN tokens for a 20% APY, and a couple of dashboards with some data related to the project. Again, sparse.

One interesting tidbit is the mint page. You can mint new XEN tokens for oneself at the click of a button. A candy machine of tokens.

Source: Xen Network

The catch: these XEN tokens do not arrive immediately. In fact, the user can select how much later they can access their newly minted tokens; the minimum is set at 1 day. The longer the wait, the more tokens you get.

However, there is no guarantee that XEN will have any value in the future. If you select too long a wait you may go home empty-handed. As we said, the token does literally nothing. Not that it should matter anyway. This is crypto after all, and some of the highest-valued tokens are about as useful as an elephant in a minefield.

In any case, a lot of people are minting XEN. Like, a lot. Some have even created bots to mint new Xen from a myriad of wallets at the same time. This handy, and to some people sorta shady strategy is known as sybiling.

Could you guess who is likely the greatest sybiler of Xen? The creator of the Xen protocol itself, according to this thread. Ah, isn’t crypto fantastic?

But what concerns us today are not experimental Ponzi games.

It is the fact that ETH has turned deflationary. Let’s break this down a bit more and why this is impressive in the face of a fresh ponzi.

Burn baby, burn

The first change to the issuance of Ethereum that allowed ETH to turn deflationary was the implementation of EIP-1559 back on August 5th 2022.

EIP-1559 changed Ethereum’s fee market. The fee market refers to the way users pay fees (known as gas), and how much they pay. One needs to pay this fee for any action on Ethereum, be it a simple transfer or to interact with for instance Uniswap.

Before EIP-1559, Ethereum followed a first-price auction. This means that people bid an amount of money (in this case ETH) to pay for their transaction to be processed and the highest bidder won.

After EIP-1559, the fee is split in two: the base fee and the priority fee. The base fee is always included. The priority fee is a "tip" that users can add to get their transaction included in the next block faster.

What is interesting is that the base fee, which is denominated in ETH, is burnt. Forever.

Since the London upgrade, this is what ETH issuance looks like:

Source: ultrasound.money

The Triple Halving (of your net worth)

The second change to ETH’s issuance came thanks to the Merge, one of the most impactful events in Ethereum's history. The Merge refers to the switch from Proof-of-Work (PoW) to Proof-of-Stake (PoS) consensus, and was implemented on September 15th.

Why change to PoS? From the ethereum.org website: “ (PoS) is more secure, less energy-intensive, and better for implementing new scaling solutions”.

What the change did, too, was to reduce the amount of new ETH that is created. Before the Merge took place, ETH issuance looked like this:

Issuance to miners: ~13,000 ETH/day or ~3.95% annual inflation

Issuance to stakers: ~1,600 ETH/day or ~0.49% annual inflation

Total issuance pre-Merge: ~14,600ETH/day or ~4.44% annual inflation

After the Merge, only issuance to stakers remains:

Issuance to stakers: ~1,600 ETH/day or ~0.49% annual inflation

Total issuance post-Merge: ~1,600ETH/day or ~0.49% annual inflation

This represents an ~89% drop in issuance.

Some ethereum proponents have taken a liking to calling it the triple halving, after Bitcoin’s halving by which the issuance of BTC is cut in half every four years. Historically, this has preceded every major BTC bull market. So you can understand why investors were excited about these changes when it came to Ethereum. And many were a bit shortsighted in thinking it would happen in the weeks to follow with the Merge - this is a fundamental shift taking place with Ethereum, not a change in support/resistance like we see with short-term price movements.

Although, (drum roll please…) considering recent market conditions, the triple halving might as well have referred to a triple halving of ETH prices ($4800 -> $2400 -> $1200 -> $600). But I digress.

The fact is that the Merge dropped issuance so much that ETH can become deflationary if there is enough activity on the chain, thanks to the burn implemented by EIP-1559.

After these two changes, this is how the issuance of ETH looked like over the last 30 days:

Source: ultrasound.money

Not bad, but still inflationary.

This is because we are in the midst of a bear market, and activity on chain is very low. Which means, the base fees that were burnt were not enough to counter the 1,600 ETH that is issued every day to stakers. That is, until Xen came around.

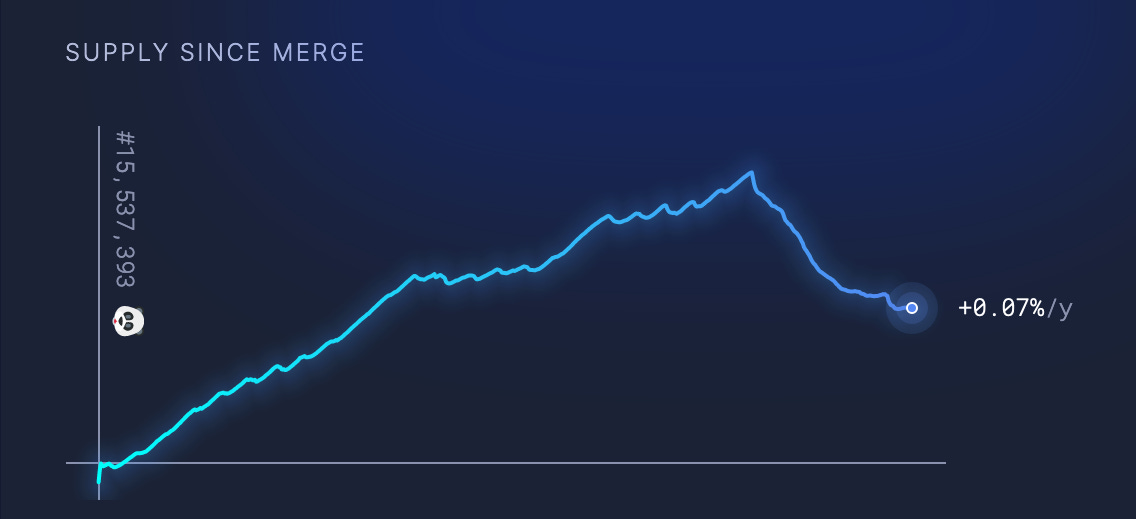

Less ETH by the minute

This is how issuance looks like over the last week, after Xen arrived to the scene:

Source: ultrasound.money

Now we are talking!

Granted, a burn of 0.17% of supply in a year does not really remove that much ETH. But look at it this way: in the past, positive issuance acted like a headwind against price appreciation. For price to go up, someone first had to gobble up all the new ETH that was being issued. Once the new ETH was purchased, existing ETH could then be purchased.

At current prices, that was $17.5M worth of ETH created each day, or over $500M a month. And most of that was given to miners that would sell it sooner rather than later.

Now, after PoS was enabled, that sell pressure is all but gone. And, if there is actual long-term deflation, that sell pressure becomes equivalent to “buy pressure”. The headwind is now a tailwind, and even investors buying Ethereum will have much more of an impact, pushing prices up much faster.

Source: ultrasound.money

Now, the team at Jarvis Labs understands this type of supply shift will be beneficial to price.

But the question on our minds is… Does this actually help the growth of the network? This is where we turn skeptical. And plan to follow up on in the months to come.

Thanks for reading.

Keep it fun,

Kodi